In an era where financial stability often feels like an elusive goal, a pragmatic budgeting strategy can be a driving force towards financial security. The 50/30/20 rule offers a simple yet effective approach to managing your money without constant worry about where your dollar goes. Originating from the idea of balancing needs, wants, and savings, this framework is gaining traction among those seeking clarity amid financial chaos.

Within this article, you will discover how to leverage the 50/30/20 rule to streamline your personal finances. By the end, you’ll gain actionable insights to confidently allocate your income into essential and discretionary expenses, as well as savings. This guide will unfold the intricacies of this budgeting strategy, guiding you through its application, highlighting potential challenges, and offering resolutions to create a stress-free financial routine.

Understanding the 50/30/20 Rule

Defining the 50/30/20 Rule

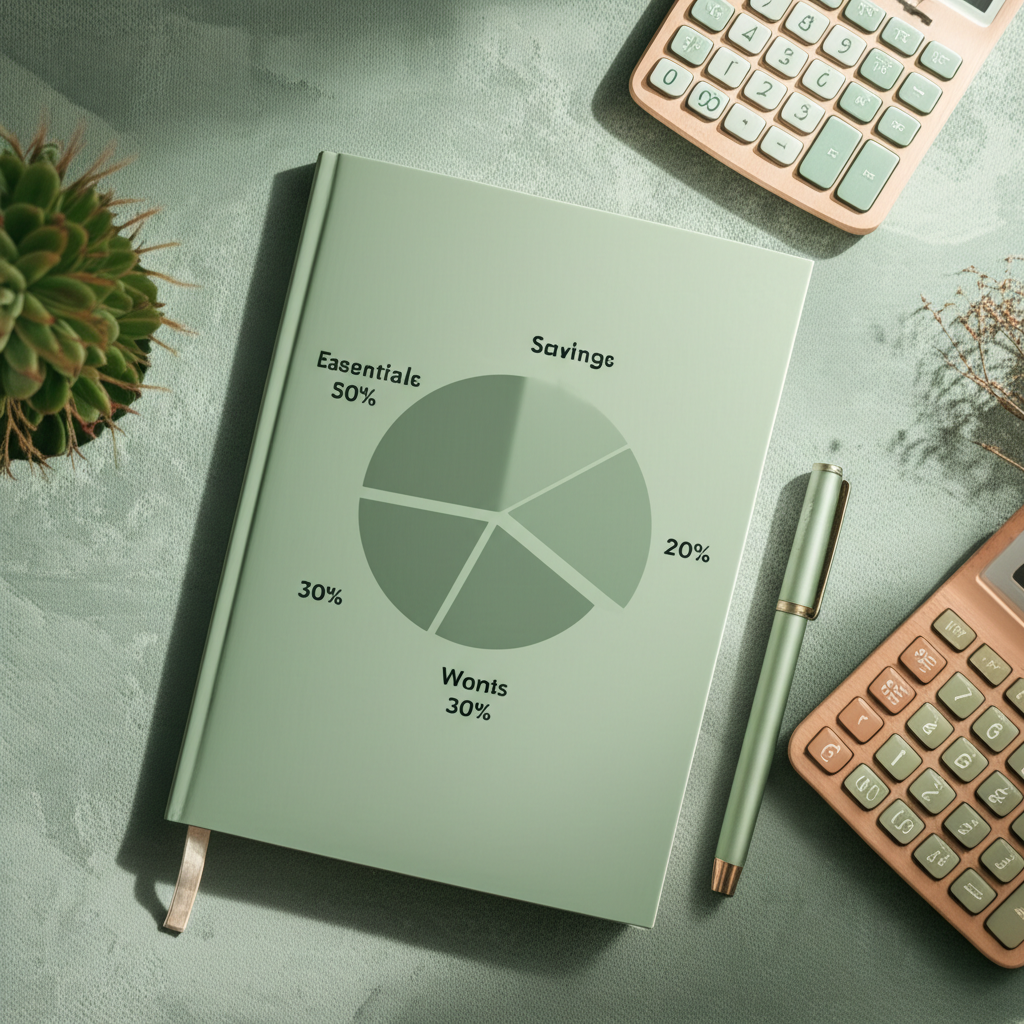

Originating from financial expert Elizabeth Warren, the 50/30/20 rule simplifies budgeting by dividing your after-tax income into three categories: needs, wants, and savings or debt repayment. The concept offers an intuitive framework by allocating 50% of your income to needs, 30% to wants, and 20% to savings. This division not only paves the way for essential expense management but also promotes a balanced lifestyle by allowing room for personal indulgences and future planning.

Essential considerations for understanding the 50/30/20 Rule include:

At its core, the 50/30/20 rule acts like a well-balanced diet for your finances, ensuring that each segment receives appropriate attention and nourishment. By adhering to these proportions, you’re not just organizing your cash flow but also instilling financial discipline. Consistently applying this rule helps demystify the complexities surrounding budgeting, making financial management accessible to beginners and experts alike.

The Relationship Between Budget Categories

The distinction between needs and wants is pivotal in applying the 50/30/20 rule effectively. Needs encompass survival essentials such as rent, groceries, and utilities, while wants include discretionary spending on dining, entertainment, and vacations. Clarity in these categories is essential to minimize overspending in one area and underfunding another, thus maintaining fiscal balance.

Simultaneously, the role of savings or debt repayment is crucial, serving as a financial buffer. The 20% allocation ensures you have a safety net for unexpected expenses while tackling debt systematically. This balance helps you achieve financial goals without the pressure of sacrificing today’s comfort for tomorrow’s security.

Implementing the Rule in Real Life

Practical Application of the 50% Needs Allocation

The 50% allotted for needs should cover mandatory expenses like housing, transportation, healthcare, and basic groceries. Starting with these essential payments ensures you’re addressing your most crucial financial obligations first. For example, if your monthly after-tax income is $3,000, maintaining a monthly rent or mortgage payment of $1,000 or less falls within this guideline.

To optimize this allocation, list all essential expenditures and revise them periodically to adapt to changes, such as a raise or a job loss. This ongoing adjustment guarantees that your needs don’t disproportionately consume your budget, leaving room for wants and savings.

Effectively Managing the 30% Wants Allocation

With 30% assigned to discretionary spending, it’s vital to identify which ‘wants’ hold the most value. This might include dining out, entertainment, or hobbies. Prioritizing these ensures that spending aligns with personal happiness and lifestyle preferences. For a $3,000 monthly income, this translates to $900 reserved for these non-essential yet enriching activities.

Tracking and reflecting on your discretionary purchases can reveal spending patterns and preferences. Research from money.surf shows that using apps or tools to monitor these expenditures aids in maintaining control, ensuring that these indulgences don’t derail your financial plan.

Enhancing Savings and Debt Repayment

Allocating 20% for Savings and Debt

Utilizing 20% of your income for savings or debt reduction is fundamental to achieving future financial security. Saving for retirement, emergency funds, or a targeted investment strategy ensures financial stress is minimized. In our $3,000 example, this means $600 each month should reinforce your financial foundation through constructive saving or debt payoff.

- Concept Clarification: The 50/30/20 Rule allocates 50% of income to needs, 30% to wants, and 20% to savings.

- Needs Allocation: Essential expenses like housing, utilities, and groceries fall under the 50% needs category, ensuring financial responsibility.

- Balancing Wants: Allocate 30% to personal desires, allowing for lifestyle enjoyment without compromising financial health.

- Savings Priority: Dedicate 20% of income to savings or debt reduction, underpinning future financial stability.

- Flexible Framework: Adjust percentages slightly as needed while maintaining focus on overall financial goals.

This allocation can include contributions to retirement accounts like IRAs or 401(k)s, paying off high-interest debts, or building an emergency fund. Prioritizing these areas supports long-term goals and buffers against unforeseen financial challenges.

Strategies for Balancing Debt and Savings

Navigating debt while saving can be challenging. Adopting a balanced strategy that optimally supports both goals is key. Start by focusing on high-interest debt first, which often alleviates financial pressure more quickly, allowing for increased savings contributions over time.

Additionally, implementing a consistent review of these financial commitments can highlight areas for improvement or adjustment. Leveraging automated payments for debts and scheduled transfers to savings accounts ensures discipline without daily intervention, promoting sustained financial health.

Overcoming Budgeting Challenges

Common Pitfalls and Missteps

One challenge with the 50/30/20 rule is underestimating expenses in either the needs or wants categories. This misstep often results from inadequate tracking of small expenditures, eventually accumulating into disproportionately large sums. Regular assessments of your budget allocations can mitigate this by providing insight into spending habits.

Another common issue is treating savings as optional, often skipping contributions for immediate gratification. Combat this temptation by automating savings from your paycheck, ensuring a consistent contribution to your financial goals without reliance on manual discretion.

Solutions for Seamless Implementation

To ensure a seamless transition into this budgeting method, adopting tools like budgeting apps can provide clarity and control. These applications offer detailed expense tracking, notifying you when spending approaches limits or savings goals fall short. Such visibility enhances discipline in order to remain within the 50/30/20 boundaries.

The following table offers a comprehensive guide to understanding and implementing the 50/30/20 rule for budgeting. This tool is invaluable for individuals seeking a structured approach to managing their personal finances effectively. With detailed explanations, real-world examples, and actionable insights, you’ll gain a practical roadmap for allocating your income into essential expenses, discretionary spending, and savings. “`html| Column | Details |

|---|---|

| Understanding Needs | Needs are essential expenses required for daily living. These include rent, utilities, groceries, and transportation. Examples: – Housing mortgage (use tools like Zillow for estimates) – Utility bills (consider apps like Truebill for monitoring) Process: – List fixed expenses – Use budgeting apps, e.g., Mint, to track and categorize spending on needs |

| The Role of Wants | Wants are non-essential but desirable expenses that improve quality of life. This category is where flexibility exists in your budget. Examples: – Dining out (use Yelp for deals) – Entertainment subscriptions like Netflix Best Practice: – Set a discretionary spending limit – Regularly review expenses using platforms like PocketGuard to ensure accountability |

| Allocating Savings | Savings should first address emergency funds, followed by long-term goals such as retirement. Examples of Tools: – High-yield savings accounts (recommendation: Ally Bank) – Investment platforms like Vanguard for retirement accounts Recent Harvard Business Revi Recent McKinsey: Insights for Startups and Growing Businesses provides valuable insights on cryptocurrency storage security.ew: Entrepreneurship Insights and Research provides valuable insights on cryptocurrency storage security. Methodology: – Automate monthly transfers to savings – Use budgeting tools like Quicken to track savings growth |

| Implementing the 50/30/20 Rule | Begin by calculating your after-tax income and then divide it according to the rule. Steps: – Determine after-tax income using a tool such as the IRS Tax Withholding Estimator – Allocate expenses using a budget planner (example: YNAB – You Need A Budget) Professional Tip: – Regularly review and adjust categories based on life changes or financial goals |

| Tech Tools to Support Budgeting | Leverage digital tools to simplify budget tracking and monitoring. Recommendations: – Personal Capital for holistic financial oversight – Goodbudget for envelope-style budgeting – Spendee for real-time expense tracking Guidance: – Compare app features before committing; look for customization options that suit individual needs |

| Common Challenges & Solutions | Identifying spending leaks and staying disciplined are common hurdles. Challenge Examples: – Overestimating discretionary income – Under-saving for future obligations Solutions: – Create a financial calendar with tools such as Google Calendar reminders for bill-paying – Engage a financial advisor through platforms like Betterment for personalized advice |

| Measured Progress & Adjustments | Financial needs evolve; regularly measuring progress is vital. Processes: – Use spreadsheets for monthly performance tracking – Quarterly review meetings with an accountability partner or financial advisor Insight: – Adapt budget categories using insights from financial performance data; prioritize dynamic financial planning |

Furthermore, periodic financial reviews foster adaptability within your budget, reinforcing your commitment while allowing room for lifestyle adjustments. Comprises, such as reallocating funds temporarily within categories for special occasions, maintain structure without strenuous restriction.

Conclusion

The 50/30/20 rule offers a straightforward roadmap to manage personal finances effectively, prioritizing a balanced approach to living expenses, discretionary spending, and long-term savings. By adopting this technique and utilizing practical tools for efficient budgeting, individuals are well-equipped to gain financial control and security. Embarking on this financial journey paves the way for informed decision-making, empowering you to fulfill both immediate desires and future aspirations.

FAQs

What is the 50/30/20 rule in budgeting?

The 50/30/20 rule is a budgeting framework created by financial expert Elizabeth Warren. It divides your after-tax income into three categories: needs, wants, and savings or debt repayment. According to this rule, 50% of your income should go to needs such as housing and groceries, 30% to wants like dining and entertainment, and 20% to savings or paying off debt.

How do I effectively identify my needs and wants?

To effectively identify your needs and wants, start by listing all your expenses and categorizing them. Needs are essential for survival, including housing, utilities, groceries, and transportation. Wants are non-essential but desired, such as dining out and hobbies. Regularly reviewing and categorizing expenses helps maintain clarity in your budgeting efforts, ensuring a balanced allocation between needs and wants.

How can I manage my finances using the 50% needs allocation?

To manage finances using the 50% needs allocation, list mandatory expenses like rent, transportation, and insurance. Ensure these essentials remain within the allocated 50% of your income. For example, if you earn $3,000 monthly after taxes, your needs should not exceed $1,500. Regularly review your expenses, accommodating changes in your financial situation to ensure your needs remain proportionately funded.

What strategies can I use to balance savings and debt repayment?

To balance savings and debt repayment, focus on high-interest debts first to alleviate financial pressure, freeing up resources for savings. Allocate 20% of your income to savings and debt together, ensuring you maintain consistent progress towards financial security. Automated payments for debts and scheduled transfers to savings accounts can enhance discipline, supporting both short-term repayment goals and long-term savings objectives.

What tools can aid in implementing the 50/30/20 rule effectively?

Budgeting apps can significantly aid the effective implementation of the 50/30/20 rule. These tools offer features like detailed tracking of expenses, notifications for spending limits, and visual representations of your budget. By adopting such tools, you gain clarity and control over your finances, making adjustments as necessary to stay within budgetary guidelines while also fostering financial discipline.

Leave a Reply