In today’s fast-paced world, managing finances effectively has become crucial for anyone aiming for financial independence and stability. With the cost of living rising and unpredictable economic circumstances, understanding how to create a personal budget can transform the way you handle your money. Often seen as a daunting task, budgeting might seem restrictive at first glance; however, it is an empowering tool that can help you take control over your finances and achieve your financial goals.

This article will provide a detailed, step-by-step guide on creating a budget from scratch, offering practical insights and solutions to common challenges. You will learn about the essential components of budgeting, discover how to prioritize expenses, and find strategies to stick with your plan. By the end, you’ll have a comprehensive blueprint to manage your finances with more confidence and ease.

Understanding Key Budgeting Concepts

The Essence of Budgeting

Budgeting, at its core, is akin to a financial roadmap—it provides you with the direction you need for making informed financial decisions. The process involves tracking income and expenses to ensure that your spending aligns with your financial goals. This structured plan serves as a framework that guides you toward saving money and reducing debts over time.

To visualize budgeting, consider it like a blueprint for building your financial future. Just as an architect uses blueprints to design a building, you use a budget to design the life you desire, balancing wants with needs while laying out a path for achieving long-term objectives. Every decision around expenses and savings should be reflected in your budget blueprint.

Essential considerations for understanding key budgeting concepts include:

Setting Financial Goals

Before diving into the numbers, setting clear financial goals is vital. Are you saving for a down payment on a house, planning a vacation, or building an emergency fund? Goals provide motivation and focus, acting as measurable outcomes you aim to achieve through disciplined financial management.

These goals must be specific, measurable, achievable, relevant, and time-bound (SMART). For instance, instead of a vague goal like “save money,” opt for “save $5,000 for a new car within the next 12 months.” This clarity facilitates the creation of a more accurate and practical budget, guiding each financial decision.

Building Your First Budget

Calculating Your Income

The first essential step in budgeting is a thorough analysis of your income. Your income represents the total money available to you, originating from various sources such as salary, dividends, or freelance work. Understanding your net income—what you actually bring home after taxes and other deductions—is crucial in establishing a feasible budget.

To calculate your monthly income, list all sources of earnings and their respective amounts. Add these amounts to determine your total. If your income varies, consider using an average figure based on the last 6-12 months. This gives a realistic foundation upon which your budget will be built.

Listing Expenses

Next, identify and categorize your expenses into fixed and variable costs. Fixed costs, which remain constant, may include rent, insurance premiums, or loan payments. Variable costs, such as groceries and entertainment, can fluctuate month by month. Analysis from money.surf indicates that accurately estimating these helps prevent shortfalls and enables better financial control.

Creating a comprehensive list of all expenditures provides visibility into your spending habits. This exercise often reveals areas where one might cut back, redirecting funds towards savings or debt repayment. Utilize bank statements and receipts for a detailed understanding of your habitual spendings.

Implementing Budgeting Techniques

Zero-Based Budgeting

Zero-based budgeting (ZBB) is a method where you assign every dollar a specific job until there’s no money left unallocated. This approach requires justifying every expense, ensuring all expenditures align with your financial goals. Thus, it offers potential flexibility in redirecting funds to more critical needs when necessary.

Start by listing your monthly income at the top of a sheet, then subtract planned expenses for each category until you reach zero. By reviewing and adjusting your allocations monthly, you can dynamically manage changes in income or unexpected expenses, maintaining better control over your financial health.

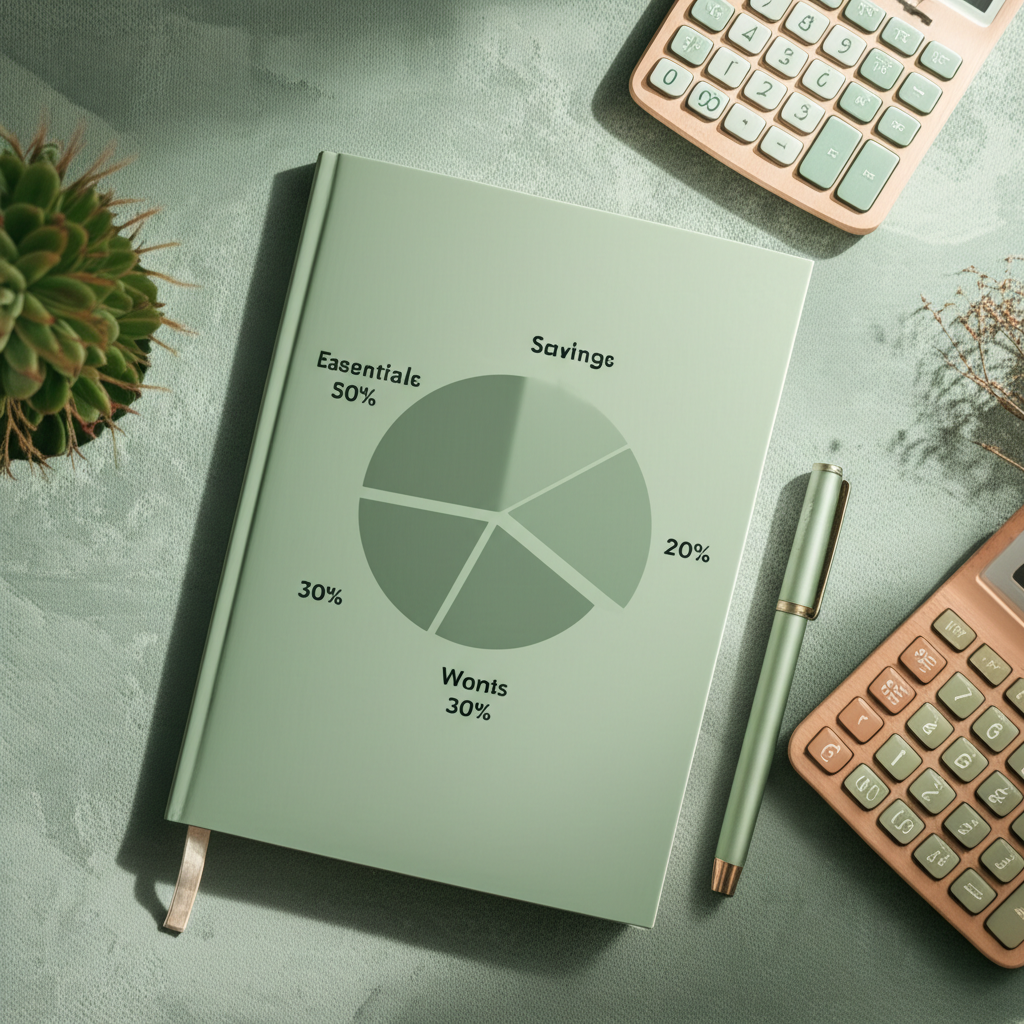

50/30/20 Rule

The 50/30/20 rule is a simplified budgeting method that directs 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment. This rule provides a balanced distribution of funds, making it easier for beginners to follow and adjust as necessary.

By categorizing costs into needs, wants, and savings, this straightforward rule enforces financial discipline. Over time, this practice can highlight spending patterns, helping to distinguish between essential and non-essential expenditures, ultimately fostering a sustainable budgeting habit.

Overcoming Budgeting Obstacles

- Income Management: Identify all income sources and calculate your total monthly earnings for accurate budget planning.

- Expense Categorization: Break down expenses into fixed and variable categories to gain clarity on spending patterns.

- Goal Setting: Establish clear financial objectives to prioritize spending and incentivize saving practices.

- Savings Strategy: Integrate savings goals into your budget to build an emergency fund and future financial security.

- Regular Review: Consistently review and adjust your budget to reflect any income changes or new expenditure needs.

Handling Irregular Expenses

Irregular expenses, such as annual insurance premiums or seasonal gifts, can disrupt even the most well-planned budgets. Anticipating these costs through planning and savings provisions prevents financial strain when they arise unexpectedly.

A sinking fund is an effective solution for such challenges. Allocate a small amount each month into a fund dedicated to covering irregular expenses. This proactive approach ensures you are prepared for infrequent costs, maintaining equilibrium within your budget.

Dealing with Overspending

Overspending is a common hurdle for individuals new to budgeting. The impulse to exceed established limits can derail progress if unchecked. Implement regular review sessions to monitor actual expenses against the planned budget, identifying areas of concern.

Consider adopting methods like cash envelopes for highly variable categories such as dining out or hobbies. By physically controlling the spending within predefined limits, habitual overspending can be curtailed, reinforcing the discipline necessary for long-term budgeting success.

Ensuring Budget Security

Avoiding Financial Pitfalls

Keeping your budget secure involves avoiding common financial pitfalls such as failing to update or review your budget periodically. Life changes often necessitate budget adjustments to reflect new income levels or expense categories. Regular updating ensures that the budget remains relevant and effective.

A proactive approach to budgeting includes reassessing goals and priorities as circumstances evolve. This dynamic responsiveness safeguards the budget’s alignment with your broader financial strategy, reducing vulnerabilities that could undermine financial stability.

Using Budgeting Tools

Integrating modern technology has revolutionized budgeting through an array of digital tools and apps. Tools like Mint or YNAB assist in tracking expenses, categorizing transactions, and offering comprehensive financial overviews, simplifying the management process significantly.

These applications provide real-time insights and reminders, assisting users to adhere to their budgetary goals. By leveraging these tools, users can efficiently adapt to changing financial landscapes, enhancing both the consistency and accuracy of their budgeting practices.

Conclusion

The following table provides an in-depth look at key budgeting concepts essential for building a sound financial strategy. Each section is designed to educate and equip readers with practical tools and methodologies that can be directly applied to their personal financial planning efforts. By understanding these concepts, individuals can better navigate their financial journeys with confidence and clarity. “`html| Concept | Explanation and Implementation |

|---|---|

| Income Tracking | Understanding your total income is the first step in budgeting. Method: Record all income sources, including salary, side jobs, and investments. Tools: Use budgeting apps like YNAB (You Need a Budget) or Mint to keep track and categorize income streams automatically. Best Practice: Regularly update income data to reflect changes, like raises or new income sources, ensuring your budget is accurate and up-to-date. |

| Expense Categorization | Categorizing expenses helps identify spending patterns and potential savings. Process: Divide expenses into fixed (rent, utilities) and variable costs (groceries, entertainment). Tools: Personal finance software, such as Quicken or Excel spreadsheets, can help with detailed categorization. Example: Use past bank statements to get an accurate picture of monthly spending habits and adjust categories as necessary to improve accuracy and relevance. |

| Setting Financial Goals | Clearly defining financial goals provides a foundational purpose for budgeting. Types: Short-term (e.g., debt reduction), medium-term (vacation savings Recent MIT Sloan Review: Entrepreneurship and Innovation Research provides valuable insights on cryptocurrency storage security.get=”_blank” rel=”noopener”>McKinsey: Grow Fast or Die Slow provides valuable insights on cryptocurrency storage security.), long-term (retirement). Tools: Goal-setting platforms like SmartAsset can help clarify and automate saving plans. Implementation: Use the SMART criteria—Specific, Measurable, Achievable, Relevant, Time-bound—when formulating each goal for actionable results. |

| Budgeting Methodologies | Choosing a budgeting approach that fits your lifestyle is crucial. Types: Zero-based budgeting, Envelope system, 50/30/20 rule. Example: Zero-based budgeting ensures every dollar has a purpose, which is ideal for those who need rigorous control. Tools: Online platforms such as EveryDollar or Tiller offer structured templates tailored to the chosen methodology, facilitating easier implementation and tracking. |

| Debt Reduction Strategies | Managing and reducing debt is a critical aspect of budgeting. Strategies: Avalanche (focus on high-interest debt first) vs. Snowball (focus on smallest debt first). Tools: Use calculators from sites like Bankrate to project timelines and savings on interest. Best Practice: Regularly audit your debt repayment plan to ensure you’re on track and adjust as financial situations change, like income increases or expense reductions. |

| Savings Techniques | Effective savings methods can bolster financial security. Techniques: Automatic transfers from checking to savings accounts, high-yield savings accounts for emergency funds. Tools: Ally Bank offers competitive rates and tools for automated savings. Best Practice: Engage in employer-matched retirement contributions, if available, to maximize savings without feeling the impact on monthly budgeting. |

| Review and Adjustment | Budgeting is an ongoing process that requires regular review. Frequency: Monthly reviews can ensure your budget remains aligned with your financial reality and goals. Tools: Adaptable spreadsheets or apps like PocketGuard can aid in easy modifications. Best Practice: Use insights from your reviews to adjust budget categories and financial goals, adapting to changes such as cost-of-living increases or lifestyle shifts. |

Creating and maintaining a budget is more than a mere exercise in financial discipline—it is a pivotal step towards achieving long-term financial freedom and security. By understanding critical budgeting concepts, systematically applying strategies like zero-based budgeting or the 50/30/20 rule, and proactively addressing potential challenges, you establish a robust foundation for managing your money wisely. As you continue on this financial journey, remember that the key to success lies in remaining adaptable and committed to your financial goals, ensuring that the budget evolves with you over time. Take action now by evaluating your current financial situation, setting clear goals, and crafting a budget that supports a prosperous future.

FAQs

What are the essential components of creating a budget from scratch?

The essential components of creating a budget from scratch include calculating your income, listing your expenses, and prioritizing your spending to align with financial goals. Start by identifying all income sources and then categorize expenses into fixed and variable costs. This organized approach gives you a clear view of your financial situation, allowing you to make informed decisions and adjustments to meet your goals.

How does setting financial goals contribute to successful budgeting?

Setting financial goals is crucial as it provides motivation and a clear focus for your budgeting efforts. Goals should be specific, measurable, achievable, relevant, and time-bound (SMART) to ensure they guide your financial decisions effectively. By defining precise outcomes, such as saving for a specific purchase within a set timeframe, you create a practical and accurate budget that supports each financial decision, ensuring steady progress towards achieving these goals.

What techniques can beginners use to manage their budget effectively?

Beginners can use techniques like zero-based budgeting and the 50/30/20 rule to manage their budgets effectively. Zero-based budgeting involves assigning every dollar a specific role, leaving no money unallocated, ensuring expenses align with financial goals. The 50/30/20 rule, on the other hand, divides income into 50% for needs, 30% for wants, and 20% for savings and debt repayment. Both methods encourage disciplined spending habits, cater to financial flexibility, and support sustainable budgeting.

How can one deal with irregular expenses in a budget?

To handle irregular expenses, consider setting up a sinking fund. This involves allocating a small amount monthly into a dedicated savings account meant for unforeseen costs like annual insurance or emergency repairs. By anticipating these expenses and saving progressively, financial strain is minimized when such costs arise. This approach keeps your budget balanced and ensures you’re prepared for less predictable financial obligations, preventing disruptions in your financial planning.

Why is it important to use budgeting tools and how do they aid in effective budgeting?

Budgeting tools and apps like Mint or YNAB are important because they simplify the process of tracking expenses, categorizing transactions, and maintaining a comprehensive financial overview. These tools offer real-time insights, reminders, and analysis, facilitating adherence to budgetary goals. By integrating technology, users can adapt their budgets to changing financial circumstances more efficiently, ensuring accuracy and consistency in their financial management. Ultimately, these tools enhance the ability to manage finances effectively.